Resources · Money

Interest Only vs Amortizing Loan

An interest only payment and an amortizing payment use the same loan amount and the same rate but cover different things each month. The interest only payment covers interest only, so the balance stays flat. The amortizing payment covers both interest and principal, so the balance steadily drops. This guide compares the two payments side by side, walks through one worked example, and points to the right calculator for each case. Run the numbers on the interest only loan calculator and the loan calculator for any specific scenario.

7 min read

Quick comparison

Interest only

Interest only loan

- Payment covers interest only

- Principal does not go down during the interest only period

- Payment is usually lower at first

- Payment may rise later when the interest only period ends

Amortizing

Amortizing loan

- Payment covers interest and principal

- Principal goes down over time

- Payment is usually higher at first than the interest only version

- Balance is scheduled to reach zero by the end of the term

What is an interest only payment?

An interest only payment is one period of interest charged on the current balance. Nothing more is added; nothing is subtracted from the principal. The same payment shows up every month for as long as the balance and the rate stay the same.

Interest only monthly payment

Monthly payment = principal × annual rate ÷ 12

The annual rate is written as a decimal, so 7 percent is 0.07. The result is the interest charge for one month on the current balance.

The full derivation lives in the interest only loan formula guide, with worked examples and edge cases. To run the formula on a specific loan in one step, use the interest only loan calculator.

What is an amortizing payment?

An amortizing payment covers both the interest that accrued during the month and a piece of the principal. The payment itself is a fixed amount, but the split inside it shifts over time. Early in the loan, most of the payment is interest because the balance is large. Later, most of the payment is principal because the balance is small. By the final scheduled payment, the balance reaches zero.

Amortizing monthly payment

M = P × r × (1 + r)^n / ((1 + r)^n − 1)

- M = monthly payment

- P = loan amount (principal)

- r = monthly rate (APR ÷ 12 ÷ 100)

- n = number of monthly payments

The longer guide for that formula is how to calculate a loan payment. For a specific loan, the loan calculator returns the payment, total interest, and payoff time at once.

Worked example

Same loan, two payment styles. Loan amount $250,000, annual rate 7 percent, term 30 years.

Interest only. Principal × annual rate ÷ 12 = 250,000 × 0.07 ÷ 12 = $1,458.33 per month. The balance after that payment is still $250,000.

Amortizing. Using M = P × r × (1 + r)^n / ((1 + r)^n − 1) with r = 0.07 ÷ 12 and n = 360, the payment works out to about $1,663.26 per month. Each month a small piece of that goes to principal, so the balance starts dropping from $250,000 right away.

Monthly difference. About $204.93. The interest only payment is lower at first because it does not reduce the principal balance. That gap pays for convenience in the short term and leaves the full $250,000 still owed at the end of the interest only period.

The interest only loan calculator includes a compare mode that runs both calculations side by side for any inputs.

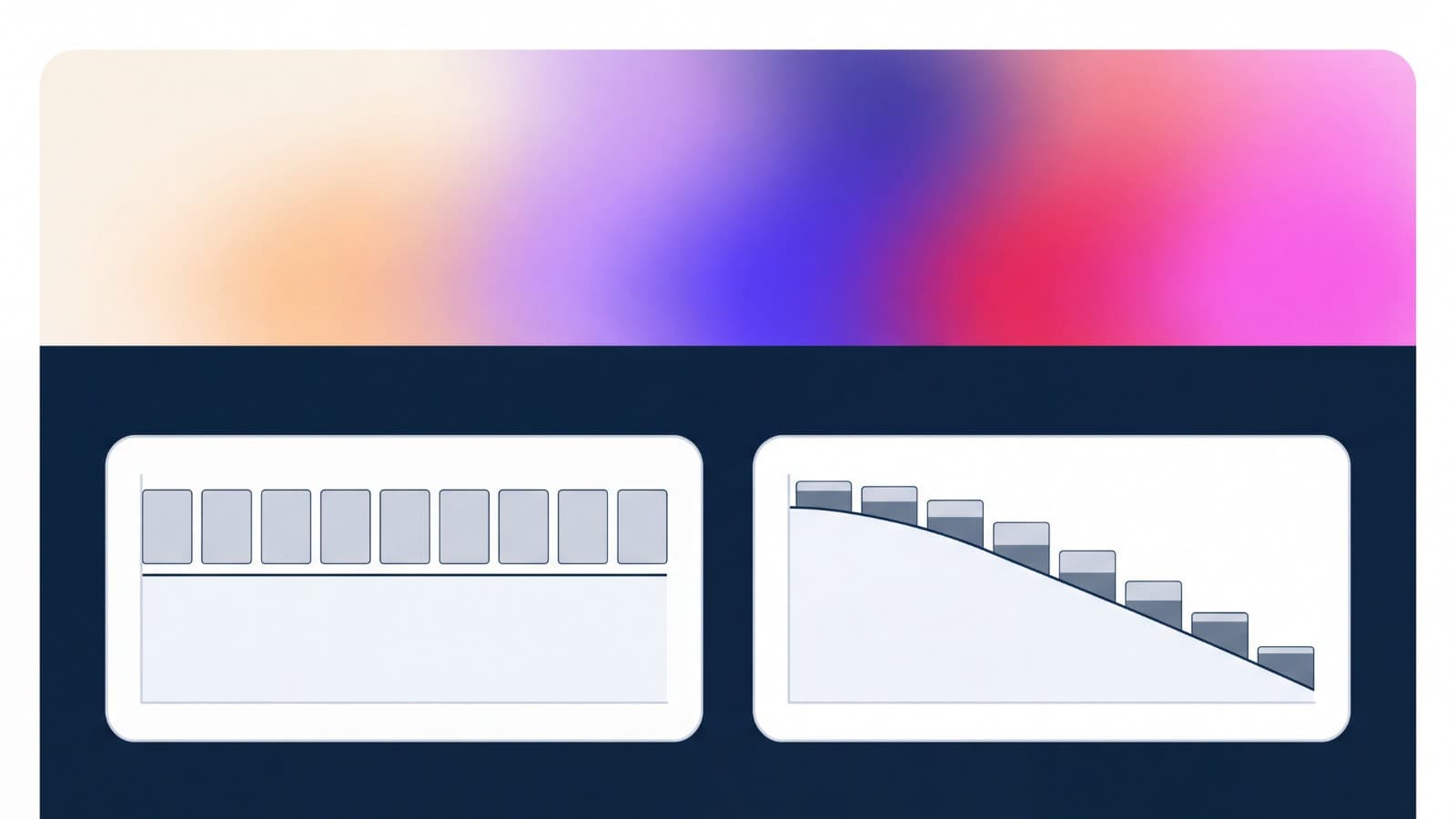

What happens to the loan balance?

The balance is the cleanest way to see the difference between the two payment types. On the same $250,000 loan at 7 percent:

- Interest only. The balance stays at $250,000 for the entire interest only period. Each monthly payment is exactly the interest charge for that month and nothing more.

- Amortizing. The balance declines a little every month, slowly at first and faster near the end. After year 1 of a 30 year amortization at 7 percent, the balance has dropped from $250,000 to roughly $247,500. After year 10 it is closer to $215,000. By the final scheduled payment it reaches zero.

Two payments of the same size on these two structures leave very different balances behind. The amortizing payment is doing two jobs each month; the interest only payment is doing one.

What happens after the interest only period?

Interest only loans almost always end with a transition. What happens at that point is set by the loan contract, not by the formula, and it varies by lender. The common outcomes are:

- Payment resets to amortizing. The full balance starts amortizing over the remaining term. Because the principal has not been paid down, the new payment is higher than what the same loan would have cost as a regular amortizing loan from day one.

- Balloon payment. The entire remaining balance is due in a single payment on a specific date. Some commercial and bridge loan contracts work this way.

- Refinance. The borrower takes out a new loan that pays off the old one. Whether this is available, and on what terms, depends on the rate environment, the borrower's credit profile, and the lender's rules at that time.

None of these outcomes is automatic. The exact terms, fees, and timing are written into the original loan agreement.

Common mistakes

- Assuming interest only means cheaper overall. The monthly payment is lower; the lifetime cost usually is not.

- Forgetting that principal is not being paid down during the interest only period. The balance is unchanged until something else pays it.

- Comparing only the first month's payment. The comparison only makes sense across the full horizon of both loans, including whatever happens after the interest only period ends.

- Ignoring fees, escrow, property taxes, homeowners insurance, PMI, and HOA on a mortgage. None of those are in the principal-and-interest payment, but all of them are part of the total monthly cost.

- Overlooking adjustable rate features. If the rate can change during or after the interest only period, both payment figures will change with it.

- Assuming every lender handles the end of the interest only period the same way. Reset, balloon, and refinance all exist; the contract decides which.

Which calculator should you use?

Pick the calculator that matches what you are trying to answer. The same loan amount and rate can go into more than one of these, depending on the question.

Interest Only Loan Calculator

Interest only payment math on any loan amount, rate, and frequency, plus a side-by-side amortizing comparison.

Loan Calculator

Standard amortizing loan payment with optional extra payments and a full interest total.

Mortgage Calculator

Principal and interest plus property tax, insurance, PMI, and HOA dues for a full housing payment.

Simple Interest Calculator

Plain simple interest math on any principal, rate, and time period.

The rest of the money calculators cover related questions for payments, interest, and savings.

Frequently asked questions

An interest only payment covers only the interest that accrues during the period; the loan balance stays the same. An amortizing payment covers both interest and principal, so a piece of every payment reduces the balance. By the end of an amortizing term, the balance reaches zero. By the end of an interest only period, the balance is still the original loan amount unless something else paid it down.

The monthly payment is lower during the interest only period because no principal is being paid. Total cost across the life of the loan is usually higher, because the balance is not shrinking during that period and interest keeps accruing on the full amount. Whether either structure is the right fit depends on the specific contract and the borrower's situation; this guide does not give that recommendation.

No. An interest only payment is sized to cover only one period of interest. None of it goes to principal. The balance stays flat for as long as the loan is interest only and no extra principal payment is made.

One of three things, depending on the loan contract. The payment may reset to a fully amortizing schedule, which raises the monthly payment so the remaining balance is paid off over the remaining term. The loan may end with a balloon payment that pays the full remaining balance in one lump sum. Or the borrower may refinance into a new loan. The actual outcome is set by the contract, not by the formulas.

Pick the same loan amount, the same rate, and the same overall horizon, then compute each payment separately. For interest only, use principal × annual rate ÷ 12. For amortizing, use the standard formula M = P × r × (1 + r)^n / ((1 + r)^n − 1). The interest only loan calculator and the loan calculator on this site will produce both figures for any inputs you enter.