Resources · Money

How to Calculate a Loan Payment

A loan payment is the fixed monthly amount that pays down a loan over a set term. The math behind it is the standard amortized loan payment formula, which splits each payment into interest and principal until the balance reaches zero on the last scheduled payment. This guide walks through the formula, the step by step calculation, a worked example, and how extra payments change the result.

7 min read

What a loan payment includes

On a fixed-rate amortizing loan, every monthly payment is the same size. Inside each payment, the split between principal and interest shifts over time: early payments are mostly interest because the balance is large, and later payments are mostly principal because the balance is small. By the last payment, the balance has been paid down to zero.

The fastest way to see this in action is the loan calculator. Enter the loan amount, the APR, and the term, and the scheduled payment, total interest, and payoff time are ready instantly. The rest of this guide explains where the number comes from.

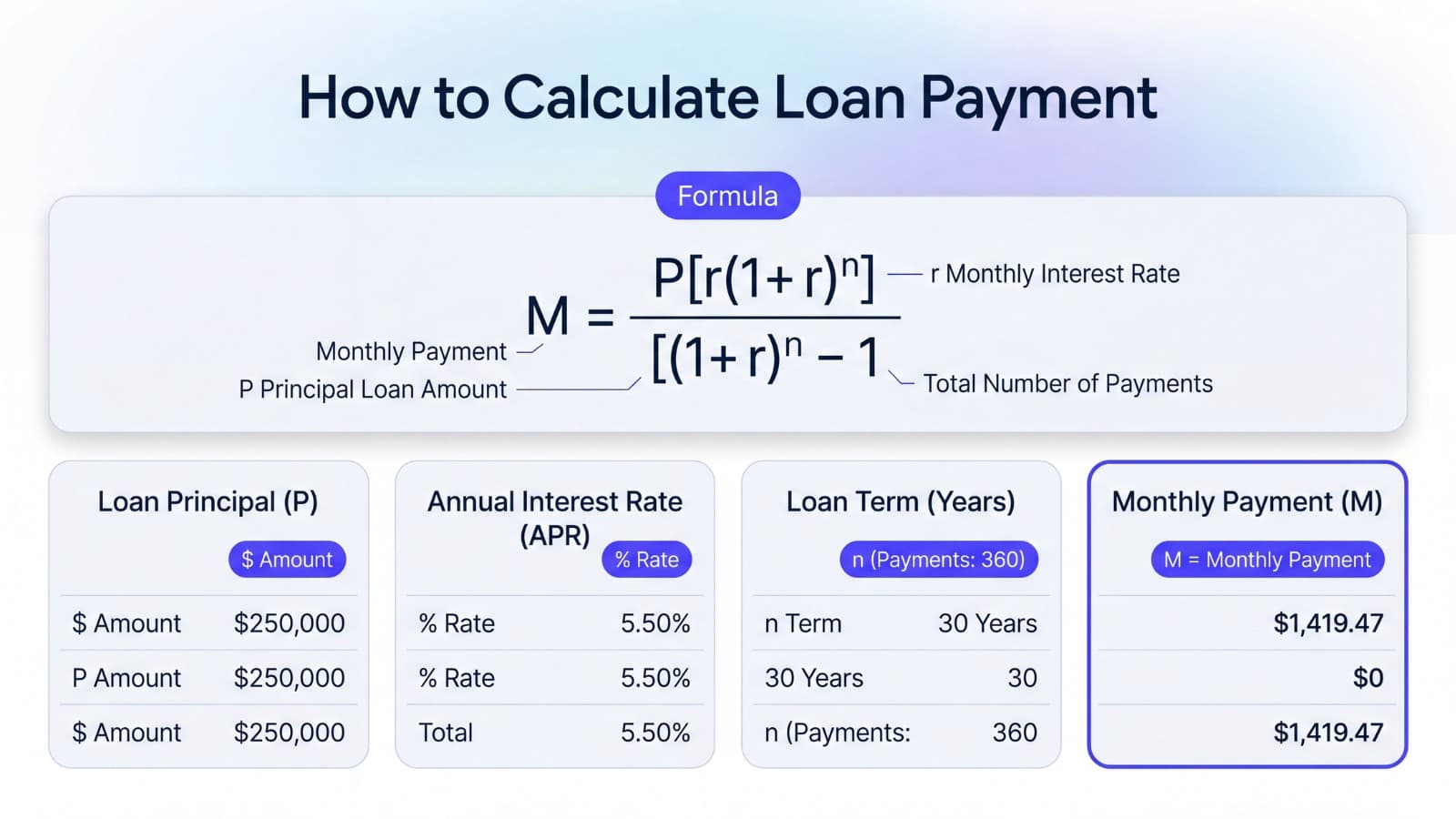

The loan payment formula

The standard amortized loan payment formula is short to write and a little dense to read. The two formulas below cover the normal case and the special case where the rate is zero.

Monthly loan payment

M = P × r × (1 + r)^n / ((1 + r)^n − 1)

The parts

- M = monthly payment

- P = loan amount (principal)

- r = monthly interest rate (APR ÷ 12 ÷ 100)

- n = number of monthly payments

At 0 percent APR

M = P / n

How to calculate a loan payment step by step

- Convert APR to a monthly rate. Divide APR by 12, then by 100 to get the monthly rate r as a decimal. For 8 percent APR, r = 8 ÷ 12 ÷ 100 ≈ 0.006667.

- Find the number of monthly payments. Multiply the term in years by 12. A 5 year loan has 60 monthly payments.

- Plug into the formula. Compute (1 + r)^n once, then use the result in both the numerator and the denominator.

- Round the monthly payment. Round to the nearest cent. The total interest is the monthly payment times n, minus the loan amount.

Worked example

Loan amount $10,000, APR 8 percent, term 5 years (60 monthly payments).

- r = 0.08 ÷ 12 ≈ 0.006667

- n = 5 × 12 = 60

- (1 + r)^60 ≈ 1.489846

- Numerator: 10,000 × 0.006667 × 1.489846 ≈ 99.323

- Denominator: 1.489846 − 1 = 0.489846

- M ≈ 99.323 ÷ 0.489846 ≈ $202.76 per month

The totals fall out from there:

- Total of payments = 202.76 × 60 ≈ $12,165.84

- Total interest = 12,165.84 − 10,000 ≈ $2,165.84

The loan calculator produces the same numbers for these inputs.

How extra payments change payoff time

An extra monthly payment goes straight to principal because the interest portion is already covered by the scheduled payment. That shrinks the balance, which shrinks next month's interest, which lets a bigger slice of the next scheduled payment go to principal too. The effect compounds, and the loan pays off well ahead of schedule.

With the same $10,000 loan at 8 percent for 5 years, adding $50 per month on top of the scheduled $202.76 cuts the payoff from 60 months down to about 47 months. Total interest drops from $2,165.84 to roughly $1,648, saving about $518 with about 13 months of payments saved as well. Even modest extra payments add up.

APR and loan term

APR is the annualized cost of borrowing and includes the interest rate plus, in many cases, a few fees. The formula here uses APR converted to a monthly rate. If a lender quotes only a rate without fees, that rate and APR can differ. Either way, the bigger the rate, the bigger the payment and total interest.

Loan term works in the other direction. Longer terms lower the monthly payment but raise total interest. Shorter terms raise the monthly payment but lower total interest. The right term depends on what monthly payment you can comfortably afford. For a percentage comparison between two scenarios, the percentage increase calculator can quantify the difference.

Common mistakes

- Treating APR as the monthly rate. Always divide by 12 before plugging into the formula.

- Picking a long term just to lower the monthly payment without checking the total interest you would pay over the term.

- Forgetting that fees rolled into the loan also earn interest over the life of the loan.

- Assuming an extra payment that doesn't exceed the monthly interest will move the payoff. The extra has to actually reduce principal to help.

- Confusing rate and APR on loans with fees. They are usually close on personal loans but can differ.

Frequently asked questions

The standard amortized loan payment formula is M = P × r × (1 + r)^n / ((1 + r)^n − 1). M is the monthly payment, P is the loan amount (principal), r is the monthly interest rate (APR ÷ 12 ÷ 100), and n is the number of monthly payments. The same formula is used for personal loans, auto loans, student loans, and mortgages.

First, convert the APR to a monthly rate by dividing by 12 and then by 100. Second, multiply the term in years by 12 to get the number of monthly payments. Third, plug those numbers along with the loan amount into the formula above. Doing this in a spreadsheet with the PMT function gives the same answer.

A higher APR raises both the monthly payment and the total interest paid over the term. Even a small change of half a percent can move the payment by several dollars and add hundreds or thousands of dollars in total interest over multi-year loans. APR is the annualized cost of the loan; the monthly rate is APR ÷ 12.

A longer term spreads the loan across more months, which lowers the monthly payment but raises total interest because the balance is outstanding longer. A shorter term raises the monthly payment but lowers total interest. The shortest term you can comfortably afford usually wins on total cost.

At 0 percent APR the standard formula simplifies to M = P / n. Each payment is the loan amount divided by the number of months, and no interest is paid. Promotional 0 percent offers from lenders sometimes have other fees, so check the full loan terms before assuming the cost is zero.

Every dollar of extra payment goes straight to principal. That lowers the balance future interest is calculated on, so the payoff arrives earlier and total interest drops. Even a small extra amount each month can shave months off the loan and save real money in interest.

The principal and interest portion of a mortgage uses the same formula. A full mortgage payment also includes property tax, homeowners insurance, and sometimes PMI and HOA dues. For the principal and interest piece alone, the math is identical to a plain loan.