Resources · Money

How to Calculate a Mortgage Payment

A monthly mortgage payment has more moving parts than a plain loan. There is the principal and interest piece, which uses the standard amortization formula, and then there are the taxes, insurance, and any PMI or HOA dues that round out the full housing payment. This guide walks through both pieces, with a worked example using realistic defaults.

8 min read

What a mortgage payment includes

A typical monthly housing payment has up to five pieces: principal and interest on the loan itself, monthly property tax, monthly homeowners insurance, PMI if the down payment is under 20 percent on a conventional loan, and HOA dues if the property is in an association. The full payment is just the sum of those pieces.

The fastest way to see the full number is the mortgage calculator. Enter the home price, down payment, rate and term, plus the annual tax and insurance and any PMI or HOA, and the calculator sums everything into one estimated total.

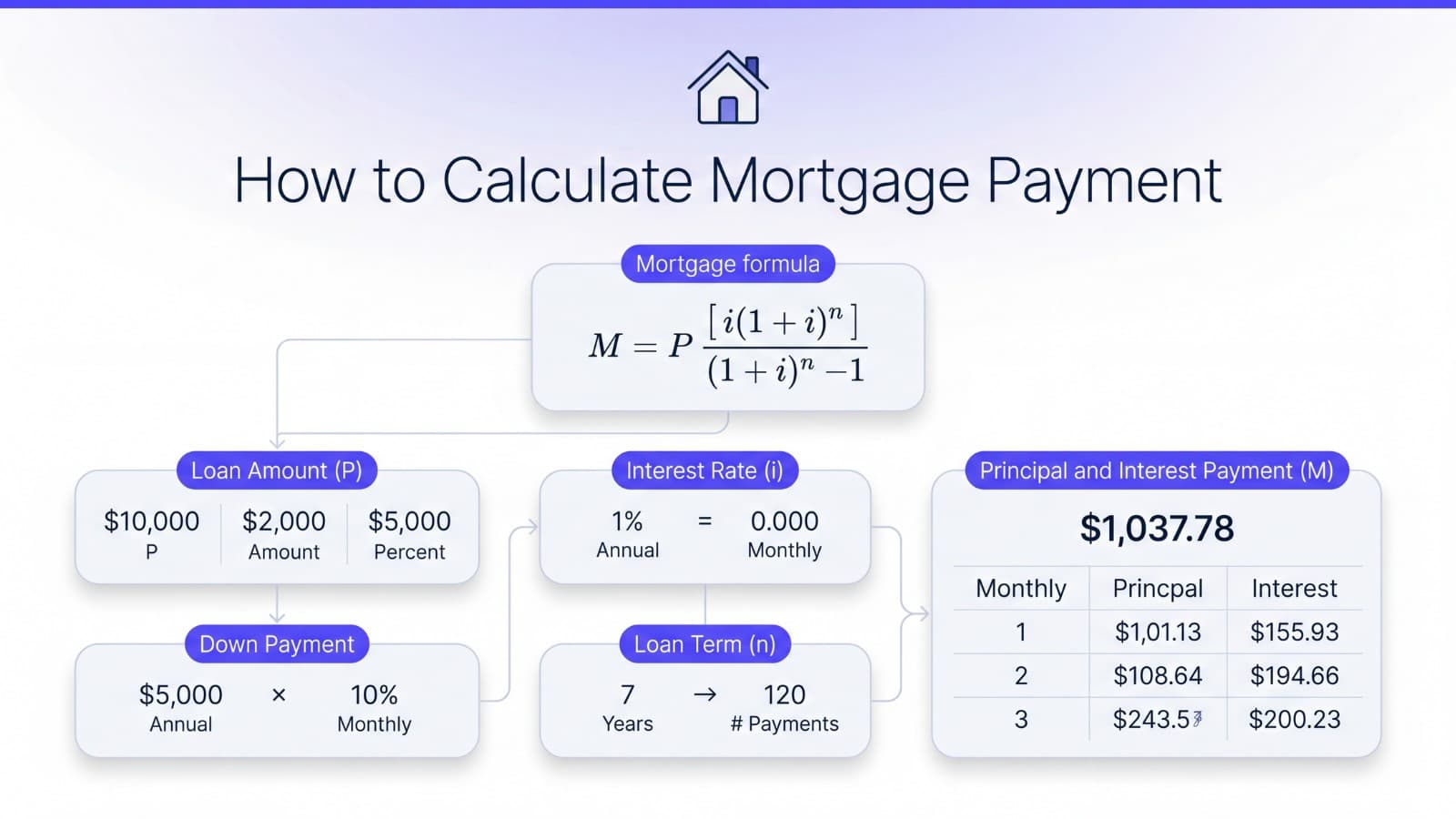

Principal and interest formula

The principal and interest portion uses the same amortized loan payment formula that auto and personal loans use. The inputs are the loan amount, the monthly rate, and the number of months.

Monthly principal and interest

M = P × r × (1 + r)^n / ((1 + r)^n − 1)

The parts

- M = monthly principal and interest payment

- P = loan amount (home price − down payment)

- r = monthly interest rate (rate ÷ 12 ÷ 100)

- n = number of monthly payments

Full monthly housing payment

total = M + tax/mo + insurance/mo + PMI + HOA

At 0 percent interest

M = P / n

How to calculate a mortgage payment step by step

- Compute the loan amount. Subtract the down payment from the home price.

- Convert the rate. Divide the interest rate by 12 and then by 100 to get the monthly rate r as a decimal.

- Count the months. Multiply the term in years by 12. A 30 year mortgage has 360 monthly payments.

- Run the formula. Compute (1 + r)^n once, then use it in both the numerator and the denominator to get the principal and interest payment.

- Add taxes and insurance. Divide the annual property tax and the annual homeowners insurance premium by 12, and add both to the principal and interest payment.

- Add PMI and HOA if any. Add the monthly PMI premium and any HOA dues to get the full estimated housing payment.

Property taxes and home insurance

Property taxes are paid to the local government, typically as a percentage of the assessed home value. Rates vary widely by state and county, so the calculator asks for the annual amount rather than guessing a rate. Homeowners insurance protects the property against covered damage. Both are usually billed yearly but split into 12 monthly amounts on the mortgage statement, often through an escrow account that the lender manages.

PMI and HOA dues

PMI typically applies when the down payment is under 20 percent on a conventional mortgage. It is usually billed monthly and can often be removed once the borrower reaches 20 percent equity through paying down the loan or appreciation. HOA dues are paid to a homeowners association if the property is in one, and pay for shared maintenance and amenities. Both are entered as monthly amounts and added directly to the housing payment.

Worked example

Home price $350,000, down payment $70,000, loan amount $280,000, interest rate 7 percent, term 30 years, property tax $4,200 per year, home insurance $1,800 per year, no PMI, no HOA.

- Loan amount: 350,000 − 70,000 = $280,000

- r = 0.07 ÷ 12 ≈ 0.005833

- n = 30 × 12 = 360

- (1 + r)^360 ≈ 8.116497

- Principal and interest: 280,000 × 0.005833 × 8.116497 ÷ 7.116497 ≈ $1,862.85 per month

- Property tax: 4,200 ÷ 12 = $350.00 per month

- Insurance: 1,800 ÷ 12 = $150.00 per month

- Total monthly payment: 1,862.85 + 350 + 150 + 0 + 0 ≈ $2,362.85

The totals over the full term follow from there:

- Total of principal and interest payments ≈ $670,624.92

- Total interest ≈ $390,624.92

The mortgage calculator produces these same numbers for these inputs.

Mortgage payment vs full housing payment

The phrase mortgage payment is often used loosely. Some people mean only the principal and interest piece. Others mean the full housing payment with taxes, insurance, PMI, and HOA. When comparing offers, make sure both sides are quoting the same number. A loan with a lower principal and interest payment but a high HOA can still cost more each month than a loan with higher principal and interest and no HOA.

To compare two interest rate scenarios in percentage terms, the percentage increase calculator can help.

Common mistakes

- Confusing principal and interest with the full housing payment.

- Forgetting PMI when the down payment is under 20 percent. Even a small monthly PMI premium adds up over years.

- Using a 15 year payment to budget a 30 year loan or vice versa. The two payments are very different even at the same rate.

- Confusing the note rate with APR. APR includes some financing fees; the rate used in the formula here is the note rate.

- Ignoring closing costs. They are not in the monthly payment but they are a real cost of buying a home.

Frequently asked questions

The principal and interest portion uses the standard amortized loan payment formula: M = P × r × (1 + r)^n / ((1 + r)^n − 1). P is the loan amount (home price minus down payment), r is the monthly interest rate, and n is the number of monthly payments. A full monthly housing payment also adds monthly property tax, homeowners insurance, PMI when it applies, and HOA dues if any.

A typical full housing payment includes principal and interest on the loan, monthly property tax (often held in escrow), monthly homeowners insurance (often held in escrow), private mortgage insurance when the down payment is under 20 percent, and HOA dues if the property is in an association. Some people call this combined payment PITI plus HOA.

Subtract the down payment from the home price to get the loan amount. Convert the interest rate to a monthly rate by dividing by 12 and then by 100. Multiply the term in years by 12 to get the number of monthly payments. Then plug those numbers into the amortized loan payment formula.

Take the annual property tax and divide by 12 to get the monthly amount. Do the same for the annual homeowners insurance premium. Add both to the principal and interest payment. Many lenders collect these through an escrow account, then pay the bills when they come due.

PMI (private mortgage insurance) is an insurance premium that conventional lenders typically require when the down payment is under 20 percent. It protects the lender, not the buyer. PMI is usually billed monthly and can often be removed once the borrower reaches 20 percent equity. Government-backed loans handle mortgage insurance differently.

A larger down payment reduces the loan amount, which directly lowers the monthly principal and interest payment and the total interest paid over the life of the loan. A down payment of 20 percent or more also typically removes the need for PMI, which can save another monthly amount.

A higher rate raises both the monthly principal and interest payment and the total interest paid. The effect compounds over a long term because interest accrues every month for 360 months on a 30 year mortgage. Even a small rate move of half a percent can add or remove tens of thousands of dollars in total interest.

No. This formula estimates the monthly payment on a specific scenario. A home affordability calculator works backward from your income, debts, and target debt-to-income ratios to suggest how much home you might afford. For affordability, also factor in closing costs, maintenance, and your local cost of living.