Resources · Money

How to Calculate a Car Payment

A car payment combines a loan and a sales tax. The loan piece uses the standard amortized loan payment formula. The sales tax piece depends on your state and whether you have a trade in. This guide walks through both, with a worked example using realistic defaults.

7 min read

What a car payment includes

The monthly car payment you make to the lender covers the amount financed plus interest. The amount financed is not just the sticker price: it is the vehicle price minus your down payment and any trade in, plus the sales tax and any rolled-in fees. After the loan starts, each monthly payment is the same size, split between interest and principal in a ratio that shifts over time.

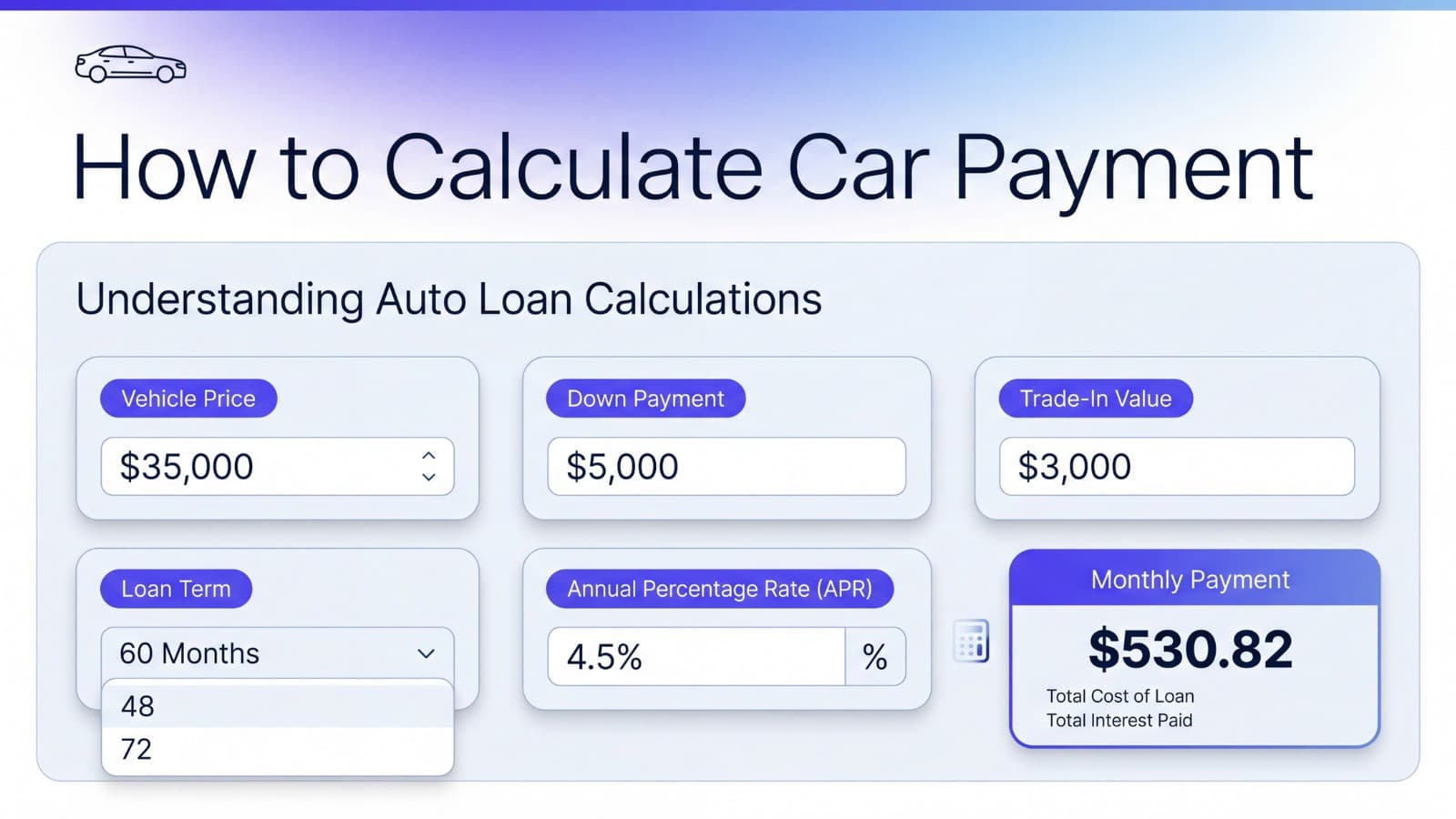

The fastest way to see the numbers is the car payment calculator. Enter the price, down payment, trade in, sales tax, term, APR, and fees, and the result and breakdown are ready instantly.

The car payment formula

The car payment is the amortized loan payment, applied to the amount financed.

Amount financed

amount financed = vehicle price − down payment − trade in + sales tax + fees

Monthly car payment

M = P × r × (1 + r)^n / ((1 + r)^n − 1)

The parts

- M = monthly payment

- P = amount financed

- r = monthly interest rate (APR ÷ 12 ÷ 100)

- n = number of monthly payments

At 0 percent APR

M = P / n

How to calculate a car payment step by step

- Start with the vehicle price. Use the negotiated price, not the sticker.

- Subtract down payment and trade in. The result is the loan amount before tax.

- Compute sales tax. Multiply the vehicle price minus the trade in by the sales tax rate. In most U.S. states, the trade in lowers the taxable base.

- Add tax and fees. Add the sales tax and any rolled-in fees to the loan amount before tax to get the amount financed.

- Run the loan formula. Convert APR to a monthly rate, multiply the term in months by 1, and plug everything into the amortization formula.

- Compute totals. Total of payments is M times n. Total interest is the total of payments minus the amount financed. Total cost is total of payments plus the down payment.

Down payment and trade in value

Both reduce the amount financed dollar for dollar. A down payment is cash out of pocket; a trade in is the dealer's credit for your old vehicle. In many U.S. states the trade in value is also subtracted from the taxable price, which lowers the sales tax bill as well, so a trade in can save money in two places at once.

Sales tax and fees

Sales tax in the U.S. is set at the state and local level. Combined rates typically range from 0 percent to over 10 percent. Most states tax the vehicle price minus the trade in value. Title, registration, and document fees are usually small but can be rolled into the loan, in which case they accrue interest over the term. For checking just the tax portion of any amount, the sales tax calculator does it in one step.

APR and loan term

APR is the annualized cost of the loan. A higher APR raises both the monthly payment and the total interest paid. Term works in the other direction: longer terms lower the monthly payment but raise total interest because the balance is outstanding longer. For a percentage comparison between two APR scenarios, the percentage increase calculator can put the difference in plain terms.

Worked example

Vehicle price $30,000, down payment $3,000, trade in $0, sales tax 6 percent, loan term 60 months, APR 7 percent, fees $0.

- Sales tax: 30,000 × 0.06 = $1,800

- Loan amount before tax: 30,000 − 3,000 − 0 = $27,000

- Amount financed: 27,000 + 1,800 = $28,800

- r = 0.07 ÷ 12 ≈ 0.005833

- n = 60

- (1 + r)^60 ≈ 1.417625

- M ≈ 28,800 × 0.005833 × 1.417625 ÷ 0.417625 ≈ $570.27 per month

The totals over the term follow from there:

- Total of payments ≈ $34,216.47

- Total interest ≈ $5,416.47

- Total cost incl. down payment ≈ $37,216.47

The car payment calculator produces these same numbers for these inputs.

Car payment vs total cost

The monthly payment is what hits your budget each month, but it is not the total cost of buying the car. Total cost includes every monthly payment over the loan plus the down payment. When comparing two offers, compare the total cost, not just the monthly payment. A loan with a smaller payment but a much longer term can easily cost more in total than a loan with a higher payment and a shorter term.

Common mistakes

- Forgetting that taxes and fees rolled into the loan also accrue interest.

- Picking a longer term to lower the monthly payment without checking how much extra total interest that costs.

- Quoting APR and monthly interest rate as if they were the same number. Monthly rate is APR divided by 12.

- Ignoring the down payment when comparing total cost between offers.

- Confusing loan amount before tax with amount financed. The amount financed adds the sales tax and any rolled-in fees.

Frequently asked questions

The principal and interest portion uses the standard amortized loan payment formula: M = P × r × (1 + r)^n / ((1 + r)^n − 1). P is the amount financed, r is the monthly interest rate (APR ÷ 12 ÷ 100), and n is the number of monthly payments. The amount financed is the vehicle price minus the down payment and trade in, plus sales tax and any rolled-in fees.

Start with the vehicle price. Subtract the down payment and the trade in value to get the loan amount before tax. Apply the sales tax rate to the vehicle price minus the trade in (the common state rule) to get the tax. Add the tax and any fees to the loan amount before tax to get the amount financed. Then plug the amount financed, the monthly rate, and the number of months into the amortization formula.

A down payment is cash you put in up front. It reduces the amount financed, which directly lowers the monthly payment and the total interest paid. A larger down payment also lowers the risk of being upside down on the loan if the car loses value faster than the balance is paid down.

A trade in works like a down payment in cash terms: it reduces the amount financed. In many U.S. states, the trade in value is also subtracted from the taxable price, so a trade in can lower the sales tax bill too.

APR is the annualized cost of the loan. A higher APR raises both the monthly payment and the total interest paid. Auto APRs depend on credit profile, term, and the lender. Even a one percentage point change can move the monthly payment by several dollars and add hundreds of dollars in total interest over a typical term.

A longer term lowers the monthly payment but raises total interest because the balance is outstanding longer. A 72 or 84 month auto loan can also leave the borrower owing more than the car is worth for much of the term. Pick the shortest term that fits the budget.

It usually does. If sales tax is financed as part of the loan, the tax is added to the amount financed and earns interest along with the rest of the balance. This guide and the calculator follow that common case.

Amount financed is the loan principal: vehicle price minus down payment and trade in, plus sales tax and any rolled-in fees. Total cost includes the down payment plus every monthly payment over the life of the loan. Total cost is what the car actually costs in dollars out of pocket, while amount financed is just what you borrowed.